The State and Local Government Procurement Snapshot for Q1 2026

For governments and businesses involved in the state, local and education contracting marketplace, Q1 2026 played out largely as anticipated. Following a challenging 2025, there was limited expectation of a sharp rebound, and the data reflected that reality: bid counts for state and local governments declined -4.2% compared to the same quarter last year. The market continues to operate in an environment of elevated uncertainty, which has led agencies to take a more measured and selective approach to procurement activity.

It is worth keeping the bigger picture in mind, however. Q1 has been trending downward for several years, shaped by a succession of different pressures along the way, and the current climate of federal funding instability and economic unpredictability is simply the latest headwind making it harder for the market to find its footing. This is not a sudden drop so much as a continuation of a pattern, and understanding what is driving it at any given moment matters as much as the number itself.

Below are summaries of the top-line findings for state and local contractors from the first quarter of 2026, as well as takeaways that can inform their business plans for the current quarter and rest of the year.

Highlights and Key Takeaways from Q1 2026

Recent SLED contracting market data shows a decline in bid/RFP volume, which can appear negative at first glance. However, when procurement activity is analyzed alongside spending trends, a clearer picture emerges: SLED agencies are not spending less, they are buying differently. The market is shifting toward fewer, larger, and more consolidated procurements, with total purchasing dollars continuing to grow year over year.

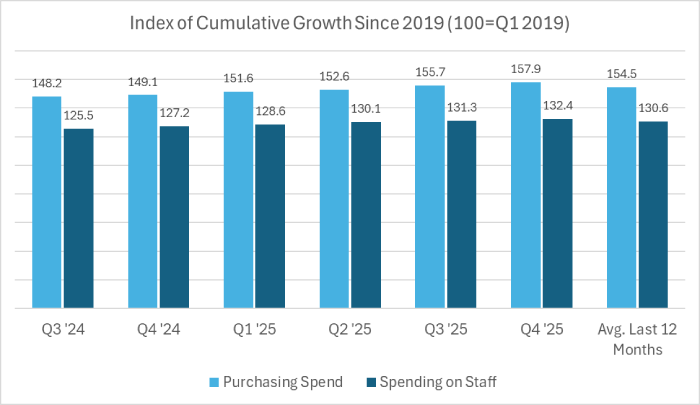

Index of Cumulative Growth

Index of Cumulative Growth

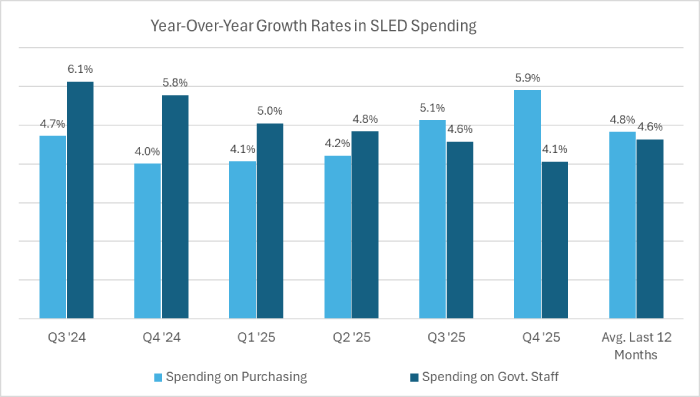

Year-Over-Year Growth Rates

Year-Over-Year Growth Rates

The above spending data are based on quarterly data available from the Bureau of Economic Analysis (BEA). Here’s what that data tells us:

Procurement Volume vs. Spending

Per our State and Local Procurement Snapshot Q1 2026 Bid/RFP counts declined roughly -4% year over year in Q1 2026, while purchasing spend continues to grow approximately +4-6% each quarter. Long-term indices indicate purchasing spend has grown more than 50 percent since 2019. This suggests agencies are issuing fewer solicitations but allocating more dollars per procurement.

Consolidation as the Primary Buying Pattern

Declining bid volume combined with rising spend indicates consolidation. Agencies are bundling projects into enterprise-wide, multi-year, or cooperative contracts, preferring vendors that can support broader scope with fewer handoffs. Vendors may see fewer opportunities overall, but larger award values.

Shift From Staffing to Contracted Capacity

Purchasing spend is growing faster than government staff spending, reflecting continued hiring constraints. Agencies are relying on vendors to extend capacity, deliver outcomes efficiently, and absorb implementation risk. End-to-end and outcome-oriented solutions align well with this environment.

More Defensive, Mission-Critical Spending

Agencies are prioritizing infrastructure, essential services, compliance-driven programs, and operational reliability. Buyers favor proven platforms, clear ROI, and low-risk implementations over experimental or discretionary investments.

Implications for Government Contractors

The bottom line is that the SLED market is not shrinking; it is becoming more selective. Vendors that adapt to consolidation, larger scopes, and stronger justification requirements will be best positioned for success.

This market rewards vendors offering enterprise-scale solutions, strong past performance, and clear value propositions. It challenges point-solution providers and volume-dependent strategies. Vendors should expect fewer bids, increased competition per opportunity, and longer but higher-value sales cycles.