Log In

Log In

Businesses that sell to state, local and education (SLED) government entities know that the market is complex and fragmented. Doing business with a major entity like the Texas State Government, for example, is much different than selling to a small school district or town.

Deltek’s team of market experts, which provides research and insight into this market for the GovWin IQ platform of government intelligence, has identified some trends that will be broadly relevant to businesses that sell across SLED governments. In the annual SLED 2023 Government Contracting Forecast on bid/RFP trends, we provided an overview of the highlights to add perspective around the prospects for continued economic recovery, amidst recession fears, in the state, local and education market.

Here are three findings that we have highlighted to share perspective on the SLED government contracting forecast for the year ahead.

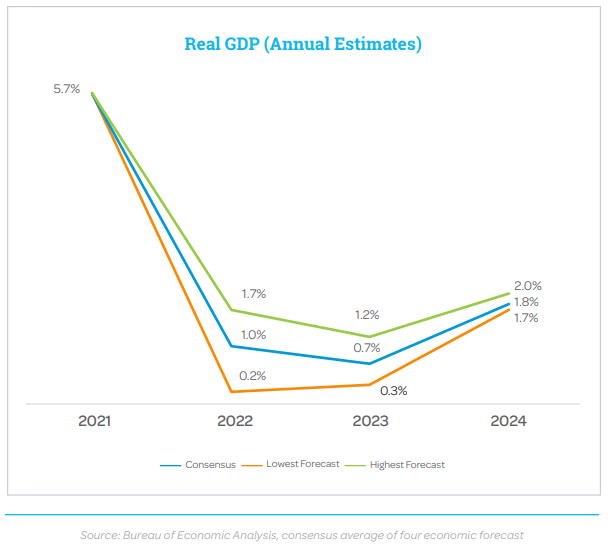

Finding #1: Economy Hits the Brakes – But Doesn’t Crash

The SLED market historically is heavily influenced by larger economic forces such as GDP (gross domestic product), business activity, investor sentiment and confidence in the future. This macro environment not only affects tax revenues but also perceptions of risk that help determine how cautious or aggressive the purchasing mood will be amongst decision makers for new advertised bids and RFPs.

After a tumultuous period in the economy during 2020 and 2021, 2022 marked a slow year of relative consistency in business activity. With many economists continuing to anticipate a recession, there is uncertainty about the future and the fiscal health of state and local governments. But SLED purchasing will likely see stabilization thanks to federal stimulus packages and the absence of a major downturn.

Our forecast anticipates GDP to grow by less than 1% in 2023 but not post an overall decline (even though it may for short periods). The Federal Reserve is hoping to have a “soft landing” in its efforts to slow the economy and reduce inflation going forward where a significant recession is avoided. While many economists expect a recession, there seems to be a consensus that it would be shallow rather than severe.

Finding #2: Most Industries Should Recover by 2024

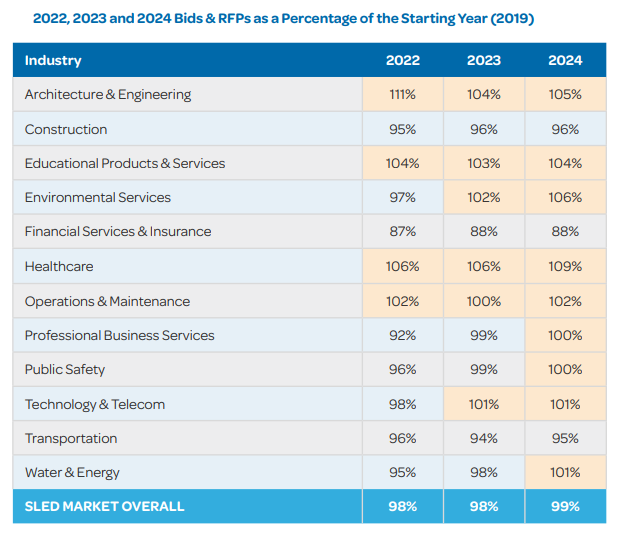

Over the next year we will continue to see more industries recover to their pre-pandemic bid numbers. While some industries have struggled to reach their original 2019 levels, others have flourished. The industries of healthcare and operations & maintenance thrived over the last two years as they provide essential services for the population and the basic operation of government.

Meanwhile, construction and professional business services fell further in 2020 and have more room to catch up. They’ve faced unique challenges as nonessential projects were put on the backburner and issues of inflation and supply chain meant fewer construction projects could be afforded on a per unit basis.

Whereas, 2022 showed strong growth for public safety, technology and environmental services, as shown above. This is representative of a market normalizing and projects that were once paused, considered non-essential, or canceled becoming a priority again. Several industries may face slower growth through 2024, such as transportation as it has struggled with depressed ridership levels for transit. However, transportation will be aided because of federal stimulus packages, providing funding for much needed infrastructure projects. In summary, the SLED market is poised to continue recovering with resilience and consistency despite the slowing economy and potential risks.

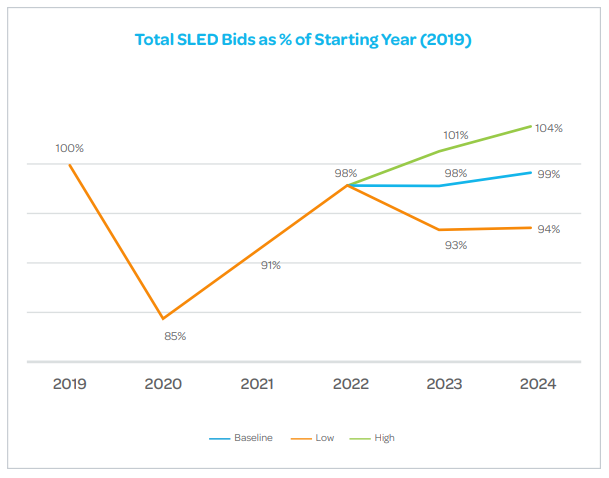

Finding #3: Alternative Forecasts Highlights Risks & Opportunities

Finally, our 2023 SLED research revealed our high and low alternative forecasts through 2024. The baseline shows bids reaching 98% of 2019 levels in 2022 extending to 99% by 2024 after being stable in 2023. The alternate forecasts provide visibility into the risks and opportunities if conditions turn out to be more pessimistic or optimistic than planned. There is a slight lean toward seeing more downside than upside risk in this forecast.

The 2022 baseline trend is pointing to a stabilizing market with federal stimulus on the horizon and the economy leveling out. Overall bid numbers for 2022 totaled just over 470,000, surpassing last year’s 439,667. Our high alternative forecast assumes there is no recession and shows the market growing to a very healthy 104%. The low alternative is a pessimistic outlook on the economy, with a recession of significant impact assumed that does not quickly rebound. In this scenario, bid levels drop to 94% through 2024, but would remain above 2021 levels.

SLED governments will no doubt be on “recession watch” and be ready to adjust any funding, bid issuance and project planning as necessary should conditions materially change. But we expect that thanks to the federal stimulus packages acting as a safety net, there will be more confidence than in prior downturns to continue typical patterns of purchasing activity.

Looking for more detailed information on the most recent quarter of SLED government activity? Download our State and Local Procurement Snapshot for Q4 2022 to get timely details on how the market is performing in industries most relevant to your business.

Deltek Project Nation Newsletter

Subscribe to receive the latest news and best practices across a range of relevant topics and industries.