With Deltek’s 2025 SLED Government Contracting Forecast report on bid/RFP trends now available, contractors have access to the highlights to add perspective on the prospects for continued recovery in the state, local and education (SLED) market amidst recession fears.

The 2025-26 bid forecast report from the experts behind the Deltek GovWin IQ government market intelligence platform provides our best estimates of how each of our 12 industries will likely trend over the next two years and what some of the big factors are that will power their growth or support their levels of demand. We work with historical trends in our statistical model but also must consider the current economy.

Build Your State and Local Sales Plan

2025 State and Local Government Contracting Forecast

Similarly, government officials who are thinking about their staff, budgets, and spending also must monitor current economic trends that ultimately affect their plans. In 2024, the SLED market experienced a period of reaction and resetting following the pandemic-induced recession and subsequent federal funding influx.

The 2024 year marked the end of broad ARPA stimulus funding, leading to a slowdown in contracting activity. Uncertainties remain, with economists offering varied predictions about the future economy. While 2024 appeared safe from a recession, there appear to be various factors contributing to a modest chance of a recession by the end of 2025.

The SLED contracting market has shown resilience, but the end of ARPA funding has reset bids to typical recession levels.

Stabilizing SLED Economic Landscape

Just as 2023 concluded with economic uncertainty for 2024, we saw 2024 ending with similar uncertainty going into 2025. GDP remained relatively steady throughout 2024 without an economic downturn. While this uncertainty persists, the data indicates a more stable and predictable economy compared to recent years with factors contributing to this stabilization. A steadying economy does not necessarily mean it will crash or thrive; it simply infers that GDP will level off, and we probably won’t see sweeping changes in interest rates and consumer spending unless a recession hits.

The conclusion of ARPA fund allocation at the end of 2024 marks the end of a period of certainty that SLED governments relied on to smooth over this transition. With further growth in revenue, many SLED governments are able to comfortably budget and prioritize funding without relying on federal funds. However, in some cases there will be painful adjustments since there is no longer an endless external reserve to draw from when funding isn’t sufficient. They must return to pre-COVID-era budgeting, where rescue stimulus funds were not an everyday safety net. This process can help push governments to stabilize their spending and distribution of funds for various products and services.

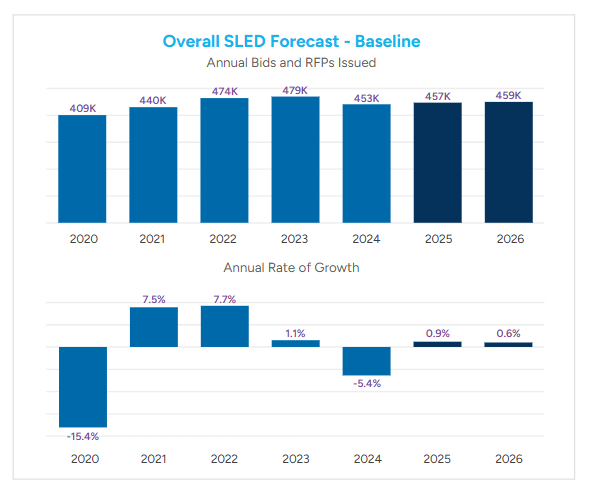

Steady Bids and Gradual Growth

Regarding bid counts, the market showed steady improvement throughout 2023, reaching approximately 479K annual bids. However, in 2024, there was a slight decline to around 453K bids, marking a 5% decrease. This downturn was initially unanticipated, as many governments were unprepared for the sudden shift away from broad ARPA funding that was needed. Despite this, it provides a basis for future forecasts. The bid count is expected to stabilize around 459K by 2026, indicating a market adjusting to the new fiscal landscape post-ARPA.

A stable and confident count of opportunities reflects the market’s relative health and bodes well for the ongoing and predictable sales revenues of contractors and suppliers. Keep in mind that the counts reflect the advertised bid/RFP part of the broader market and do not factor in the impacts of any potential increases in the rate of inflation, nor cooperative purchases and below-threshold smaller or sole source purchases acquired without a new formal bid process.

Market Reset – Thriving Beyond Federal Aid

Summarizing the twelve industries and their growth trajectory through 2026 provides insight into how each industry can thrive in the coming years. Although 2024 was a challenging year with each industry experiencing a year-over-year decline, the future looks more promising. The market’s performance in 2024 was the weakest since the pandemic-induced recession in 2020. The 2024 dip can be attributed not just to a natural course-correction from the low of 2020 but also to the rapid influx of federal stimulus — which provided immediate monetary support for SLED governments to ensure they could in fact recover fully not partly. The stimulus led to impressive growth in bids from 2021-2022, with 2023 still positive but showing signs of slowing down.

Next Steps for SLED Contractors

2024 can be seen as a market reset. The robust growth in bids during the early 2020s was unsustainable based on the size of the pandemic decline in 2020 and the length of the unusual multi-year stimulus allocations and “spend-by” deadlines. Eventually, the market needed to stabilize and return to more typical long-term patterns. This is reflected in the expected performance of the twelve industries through 2026.

While we forecast improvement in the years ahead and strength in a few industries, the growth overall isn’t likely to be significant. It paints a picture of stability as well as returning back to an era of slight growth more typical of the 1%+ annual increases since 2007 that we’ve tracked in our data set.

If you’re looking for the latest market trends to help your business earn their share of SLED government spending in 2025, download our most recent SLED procurement report below.

State and Local Procurement Report

The Latest Insights from the Q4 2024 SLED Market