In the world of finance, precision is paramount. Every transaction, every deal, every exchange leaves a trace – a financial mark that tells the story of a business’s journey. Amidst these intricate threads of financial narrative, the concept of revenue recognition emerges as a guiding light, ensuring that these threads are woven together cohesively.

Revenue recognition is more than just an accounting term; it’s the linchpin that connects a company’s operations with its financial reality.

Did You Know?In this comprehensive guide, we delve deep into the core aspects, standards, and methods that underpin this critical principle of business accounting. Through this, you’ll learn how to implement accurate revenue recognition, ensure compliance, and safeguard your business against financial pitfalls.

Improper revenue recognition can lead to significant financial missteps. According to a report by the Anti-Fraud Collaboration, the most frequent type of financial fraud that the U.S. Securities and Exchange Commission (SEC) enforced actions against was improper revenue recognition, accounting for 43% of cases over a span of 5 years.

Key Takeaways

- Revenue must be recognized when earned, not when paid: Proper revenue recognition ensures accurate financial reporting, supports compliance with ASC 606/IFRS 15, and improves business decision-making.

- Different methods apply to different service models: Approaches like percentage-of-completion, point-in-time, and over-time recognition help organizations match revenue to actual project progress.

- PSA systems improve accuracy and compliance: Polaris PSA automates revenue recognition, unifies project and financial data, and reduces manual errors compared to traditional ERP workflows.

What Is Revenue Recognition?

As a fundamental principle in financial accounting, revenue recognition dictates that the revenue of a company needs to be included in that company’s financial statements as it is earned, irrespective of the timing of cash payments. This principle ensures accurate reflection of a company’s financial performance over a specific period.

Example: Imagine a software company that provides year-long subscriptions. When a customer pays $1,200 upfront for a subscription in January, adhering to the revenue recognition principle ensures the company doesn’t immediately recognize the entire amount.

Instead, it spreads $1,200 evenly across twelve months, recognizing $100 of revenue each month. This approach accurately reflects ongoing service delivery, prevents overinflating January’s financials, and maintains transparent financial reporting.

By adhering to revenue recognition guidelines, companies aim to depict their financial reality in a way that allows stakeholders, including investors, creditors, and regulatory bodies, to gain insights into the company’s revenue-generating activities.

Why Is Revenue Recognition Important?

Even though revenue recognition is an accounting principle, it has significant implications for a company’s overall financial landscape. In this section, we explore the importance of revenue recognition compliance from a business perspective.

Strategic Decision Making

Accurate accounting as per revenue recognition is the bedrock upon which strategic decisions are built. From expansion plans to resource allocation, decisions hinge on the reliable depiction of a company's financial performance.

Investor Confidence

Transparent financial reporting is a cornerstone of investor trust. Precise accounting as per revenue recognition standards ensures that financial statements reflect a company's actual revenue-generating activities, instilling confidence in investors.

Regulatory Compliance

Adhering to revenue recognition’s stringent accounting standards, fosters regulatory compliance. Abiding by these standards safeguards against legal implications and regulatory penalties.

Accurate Performance Assessment

Proper accounting as per revenue recognition principle facilitates the accurate assessment of a company's performance. It clearly shows how well the market receives a company's offerings.

Resource Allocation

When resources are scarce, optimal allocation becomes critical. Accurate revenue recognition guides resource allocation by showcasing which revenue streams are contributing most significantly.

Growth Evaluation

Accurate revenue reporting aids in evaluating a company's growth trajectory. By identifying high-performing revenue streams, businesses can focus on scaling successful ventures.

Credible Reporting

Transparent and reliable financial reporting is pivotal for building credibility with stakeholders, including investors, creditors, and customers.

Risk Management

Proper financial reporting supports risk management efforts. It helps identify potential financial pitfalls and opportunities, enabling proactive decision-making.

Board and Executive Insights

Boards and executives rely on accurate financial insights to set direction for the business. Precise financial reporting provides a clear picture of financial health, facilitating strategic planning.

Market Perception

The way a company recognizes revenue impacts how it's perceived in the market.

Revenue Recognition Standards

Amidst the diverse landscapes of global commerce, revenue recognition standards provide the essential foundation for accurately depicting financial performance. These establish a set of rules and principles that dictate how and when revenue should be recognized in a company’s financial statements.

These standards eliminate ambiguity and subjectivity, ensuring that revenue recognition practices are robust, defensible, and in line with the economic realities of transactions.

Within this framework, the convergence of the following standards comes to the fore:

- Generally Accepted Accounting Principles (GAAP)

- Accounting Standards Codification (ASC) 606

- International Financial Reporting Standards (IFRS) 15

This contributes to a cohesive structure that guides companies in transparently recognizing and reporting revenue.

GAAP

Generally Accepted Accounting Principles (GAAP) are the bedrock of financial reporting in the United States. These encompass a set of standardized principles, guidelines, and procedures that ensure consistency and comparability in accounting practices across various industries and sectors. GAAP provides the framework companies adhere to when preparing their financial statements, including how they recognize and report revenue.

In the context of revenue recognition, GAAP sets forth principles that guide companies in determining when and how to recognize revenue from customer contracts. While GAAP doesn’t have a standalone standard solely dedicated to revenue recognition (unlike ASC 606 and IFRS 15), it includes various standards and guidelines that collectively contribute to the accurate portrayal of revenue in financial statements.

Companies following GAAP must ensure that their revenue recognition practices align with the broader principles set by GAAP, ensuring that revenue is recognized based on contractual obligations and economic realities.

ASC 606 – Revenue from Contracts with Customers

Accounting Standards Codification (ASC) 606, also known as “Revenue Recognition from Contracts with Customers”, is a pivotal milestone in revenue recognition under GAAP. This standard, issued by the Financial Accounting Standards Board (FASB), guides companies on recognizing revenue from customer contracts.

It outlines a structured approach to revenue recognition, focusing on

- identifying performance obligations,

- determining transaction prices,

- allocating revenue, and

- recognizing it as performance obligations are fulfilled.

ASC 606 ensures that revenue is recognized in a manner that aligns with contractual obligations and economic realities, enhancing transparency and consistency in financial reporting.

IFRS 15 – Revenue from Contracts with Customers

International Financial Reporting Standards (IFRS) 15, titled “Revenue from Contracts with Customers,” mirrors the collaborative spirit of ASC 606 in international financial reporting. Developed jointly by the International Accounting Standards Board (IASB) and the Financial Accounting Standards Board (FASB), IFRS 15 is the global counterpart to ASC 606.

This standard provides comprehensive guidance on revenue recognition from customer contracts under the IFRS framework. Just like ASC 606, IFRS 15 introduces a systematic approach to recognizing revenue that aligns with the transfer of goods or services to customers.

It emphasizes the importance of identifying performance obligations, determining transaction prices, and allocating revenue based on standalone selling prices.

Essential Metrics and Concepts in Revenue Recognition

In this section, we’ll explore key accounting terms and concepts that form the foundational elements of revenue recognition. These fundamental concepts and metrics are pivotal in guiding how revenue is recognized, reported, and understood within financial statements and business operations.

Annual Recurring Revenue (ARR)

ARR is a metric commonly used in subscription-based business models. It represents the annualized value of recurring subscription revenue that a company anticipates receiving from its customers.

In terms of revenue recognition, ARR can help predict future revenue streams. Still, the actual recognition of revenue would occur based on the fulfillment of performance obligations and applicable recognition criteria.

Example: A SaaS company offers a software subscription plan at $120 per year per customer. If they have 1,000 customers, their ARR would be $120,000 ($120 * 1,000).

Monthly Recurring Revenue (MRR)

Similar to ARR, MRR calculates the monthly value of recurring subscription revenue. This metric is vital for measuring the stability and growth of subscription-based businesses. It helps predict revenue streams for the upcoming months, and the recognition of this revenue follows revenue recognition principles as performance obligations are met over time.

Example: A streaming service charges its customers $10 per month for access. With 500 subscribers, the company's MRR would be $5,000 ($10 * 500).

Billings

Billings represent the total amount invoiced to customers for products or services delivered during a specific period. While billings reflect the financial transaction, revenue recognition focuses on when revenue should be recognized based on criteria like performance obligations and the transfer of control, which might not always align with billing dates.

Example: A software company signs a contract with a client for a one-year subscription, invoicing them $12,000 upfront. The billings would be recorded as $12,000, but the revenue recognition might occur gradually over the subscription period.

Bookings

Bookings indicate the total value of new customer contracts or renewals signed within a defined period. While bookings offer insights into future revenue potential, revenue recognition occurs when performance obligations are met and the criteria for recognition are fulfilled, which might not always correspond directly with booking dates.

Example: A cloud storage provider signs contracts with two new customers for $3,000 each. The bookings for the period would be $6,000, indicating the potential revenue to be recognized as the services are delivered.

Deferred Revenue

Deferred revenue, also known as unearned revenue, refers to advance payments received from customers for goods or services yet to be provided. In revenue recognition, this is recognized gradually as performance obligations are satisfied, representing a liability until earned.

Example: A training course provider receives advance payments of $2,000 from customers who register for upcoming workshops. Until the workshops are conducted, the $2,000 is considered deferred revenue, which will be recognized as and when the workshops are held.

Recognizable Revenue

Recognizable revenue refers to revenue that has met the criteria for recognition but it might not be immediately recognized due to specific timing rules. This is important for understanding when revenue should be recognized within financial statements.

Example: A consulting firm signs a contract with a client to provide services starting next month. While the services haven’t been delivered yet, the firm recognizes this as recognizable revenue in anticipation of fulfilling the contract's terms.

Recognized Revenue

Recognized revenue is the portion of revenue that meets all the necessary recognition criteria and is reported in the company's financial statements. It reflects revenue that has been earned while fulfilling all necessary conditions.

Example: A software company completes the implementation of a complex software solution for a client. Once the project is finished and the criteria for revenue recognition are met, the company recognizes the revenue earned from the project in its financial statements.

Revenue Allocation

Revenue allocation involves dividing a bundled contract's total consideration into different elements (products, services, etc.) based on their standalone selling prices. This is particularly relevant when allocating revenue to various performance obligations in multi-element arrangements.

Example: A software company offers a comprehensive software package for $1,500, which includes the base software ($1,000 standalone price), additional features ($300 standalone price), and customer support ($200 standalone price).

When a customer purchases the package, the company needs to allocate a total consideration of $1,500 among these elements based on their relative standalone prices. This ensures that revenue is recognized appropriately for each element, reflecting their individual values within the package.

Revenue Forecast

Revenue forecast is a prediction of future revenue based on historical data, market trends, and other relevant factors. While it aids in planning and decision-making, the actual recognition of revenue follows the revenue recognition principles.

Example: A smartphone manufacturer uses historical sales data, market trends, and upcoming product releases to project a revenue forecast of $10 million for the next quarter.

Realized Revenue

Revenue realization signifies recognizing revenue when it’s deemed to be realized. It means that the risks and rewards associated with ownership have been transferred to the customer as per revenue recognition criteria.

Example: An e-commerce company sells products online. It recognizes revenue when the products are shipped to customers and the title of ownership transfers to the customers, indicating revenue realization.

Revenue Variance

Revenue variance represents the difference between actual revenue and anticipated or budgeted revenue. This helps in understanding deviations from projected financial outcomes.

Example: A retail chain expected to generate $500,000 in sales for the month but actually achieved $450,000. The revenue variance in this case is -$50,000, showing a difference from the expected outcome.

Accrued Revenue

Accrued revenue is income that a company has earned but has not yet received or invoiced, reflecting the recognition of revenue on the income statement before actual cash is received. It is recorded as a current asset, usually in the form of accounts receivable, to represent the amount expected to be collected in the future.

Example: A consulting firm provides services to a client in December but does not receive payment until January of the following year. The revenue for those services would be accrued in December, even though the cash is received later. This helps in presenting a more realistic depiction of the company's financial position and performance during a specific period.

Revenue Recognition Principles or Framework

At the heart of revenue recognition lies a framework that guides companies in recognizing revenue accurately and transparently. These help in determining when and how revenue should be recorded in financial statements. This ensures consistency and comparability across different industries and transactions.

Let's explore these core revenue recognition principles with reference to an example consulting company – ABC Consulting:

Contract Identification

Begin by identifying the contract with the customer. This step sets the foundation for revenue recognition, establishing all essential terms and conditions. Contracts can take various forms, from written agreements to implied commitments. Accurate contract identification is critical as it defines the scope of revenue recognition and the obligations involved.

Imagine the consulting company, ABC Consulting, signing a written contract with a client for a year-long project. The contract outlines the scope of services, deliverables, and payment terms, establishing a clear agreement between both parties.

Performance Obligations

Clearly outline the performance obligations within the contract. These obligations represent promises to deliver goods or services, forming the basis for revenue recognition. It's crucial to identify all distinct obligations to ensure comprehensive recognition. Simultaneously, consider the inclusion of payment details to align revenue recognition with cash inflows.

This step involves evaluating the distinct nature of promised goods or services, preventing potential omissions that might affect accurate revenue recognition. Additionally, check the contract for explicit payment terms, specifying when payments are due. Aligning payment details with the fulfillment of performance obligations ensures a synchronized recognition of revenue, reflecting the business's enforceable right to payment.

For example, ABC Consulting's contract with the client includes various tasks, such as market research, strategy development, and implementation. Each of these tasks represents a distinct performance obligation, and the contract explicitly outlines payment terms, contributing to accurate revenue recognition in conjunction with the fulfillment of services.

Transaction Price Determination

Carefully determine the transaction price agreed upon in the contract. This involves considering any variable factors like discounts or incentives that affect the overall value. Accurate pricing assessment supports transparent revenue allocation. Precise transaction price determination helps avoid misunderstandings with customers and maintain consistent financial reporting.

While discussing the contract terms, ABC Consulting offers the client a 10% discount if they commit to a two-year contract instead of the original one-year term. The transaction price is adjusted to reflect this discount, ensuring that the total value accurately reflects the negotiated terms.

Allocation of Transaction Price

Distribute the transaction price accurately among the identified performance obligations. This ensures that revenue is attributed to each obligation in a fair and reflective manner. Allocation based on standalone selling prices maintains integrity in revenue distribution. Proper allocation is essential for demonstrating the value delivered to customers for each distinct obligation.

Within the contract, ABC Consulting agrees to provide both consulting services and a software solution. While the total contract value is $100,000, the standalone selling price of the software is $20,000, and the consulting services are $80,000. The transaction price is allocated accordingly to reflect the relative value of each obligation.

Satisfaction of Performance Obligations

Recognize revenue as each performance obligation is satisfied. This can occur over time as goods or services are delivered or at specific points when control transfers to the customer, aligning revenue recognition with value transfer.

Ensuring the right timing for revenue recognition enhances financial reporting precision. Properly timed recognition reflects the alignment of value delivery with financial reporting, enhancing transparency and accuracy.

ABC Consulting fulfills its performance obligations throughout the project by delivering market research, strategy development, and implementation services to the client. Revenue is recognized as each obligation is met, reflecting the transfer of value and maintaining accurate revenue reporting.

Types of Revenue Recognition Methods

Revenue recognition methods provide a structured framework for aligning revenue recognition with the actual performance of goods or services. Let's explore some common types of revenue recognition methods:

Percentage-of-Completion Method

Commonly used in construction and long-term projects, the percentage-of-completion method recognizes revenue based on the proportion of work completed relative to the total contract. This method considers costs incurred and estimates of total costs to determine the proportion of the contract completed. Revenue recognition occurs as the project advances.

As Incurred Method

This method recognizes revenue as costs are incurred, and related expenses are recognized. It’s often used in industries where costs closely align with revenue generation, such as consulting services, where revenue is recognized based on the progress of work.

Drawdown Method

The drawdown method recognizes revenue based on the incremental usage of a product or service. Revenue is recognized as customers consume or utilize their purchased capacity or usage, aligning revenue recognition with actual consumption.

Equal Distribution Method

The equal distribution method recognizes revenue evenly over a specified period. It’s often used for subscription-based models, ensuring a consistent and predictable recognition of revenue across subscription terms.

On-Invoice Recognition

Under this method, revenue is recognized at the time of invoicing, irrespective of when goods or services are delivered. It's commonly used when customers are contractually obligated to pay at the time of invoicing.

Point-in-Time Recognition

This method involves recognizing revenue at a specific point in time when a significant event occurs, indicating that control of goods or services has been transferred to the customer.

Examples of such events include the delivery of goods, completion of services, or the transfer of legal ownership. This method is applicable when the customer gains the ability to use or benefit from the product or service immediately upon transfer.

Over-Time Recognition

With the over-time recognition method, revenue is recognized gradually over the period during which performance obligations are fulfilled. This method is often employed in long-term projects or contracts where goods or services are provided incrementally. It aligns revenue recognition with the gradual transfer of value to the customer and ensures that revenue is recognized as obligations are met.

Milestone Recognition

Under this method, revenue is recognized upon reaching specific milestones or achievements outlined in the contract. These milestones could be based on completing significant project phases, achieving predetermined outcomes, or meeting specific performance criteria. This method aligns revenue recognition with the accomplishment of significant milestones rather than time-based progress.

Completed-Contract Method

In this method, revenue recognition is delayed until the entire contract is completed. It's suitable for projects where the outcome is uncertain and the ability to estimate project costs is challenging. Revenue and related expenses are recognized when the contract is fully fulfilled.

Installment Sales Method

This method is applicable when revenue is collected in multiple installments over an extended period. Revenue is recognized proportionally with each installment received. It's often used for long-term sales contracts where payments are made over time, such as equipment leasing or real estate transactions.

Cost Recovery Method

Under the cost recovery method, revenue recognition is postponed until the company recovers its costs associated with producing or delivering the goods or services. The company begins recognizing profit as revenue only after costs are covered. This approach is used when significant uncertainties exist regarding collectibility or performance.

Examples of Revenue Recognition

To solidify our understanding of revenue recognition concepts and methods, let's explore some practical examples that showcase how revenue recognition principles are applied in various scenarios. These examples illustrate the diverse ways in which companies recognize revenue, aligning with different business models and industries.

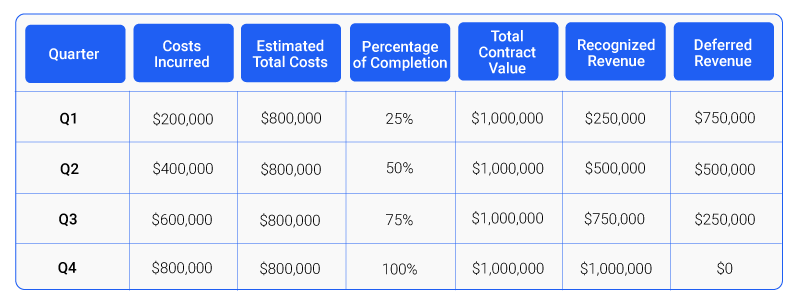

Percentage-of-Completion Method Example

Imagine a construction company, ABC Constructions, that undertakes a year-long project to build a commercial building. The total contract value is $1 million. At the end of the first quarter, the company has incurred costs of $200,000 and estimates the total costs to be $800,000.

To apply the Percentage-of-Completion method, ABC Constructions needs to calculate the percentage of work completed relative to the total contract work. This involves comparing the costs incurred to date ($200,000) with the estimated total costs ($800,000):

Percentage of Completion = (Costs Incurred to Date / Estimated Total Costs) * 100

Percentage of Completion = ($200,000 / $800,000) * 100

Percentage of Completion = 25%

With 25% of the work completed at the end of the first quarter, ABC Constructions recognizes revenue proportionally. The company recognizes revenue in line with the progress achieved, reflecting the principle of recognizing revenue as control of goods or services is transferred to the customer.

To calculate the recognized revenue, ABC Constructions applies the percentage of completion (25%) to the total contract value ($1 million):

Recognized Revenue = Percentage of Completion * Total Contract Value

Recognized Revenue = 25% * $1,000,000

Recognized Revenue = $250,000

At the end of the first quarter, ABC Constructions would recognize revenue of $250,000 based on the proportion of work completed.

Completed Contract Method Example

Consider a software company, XYZ Solutions, that specializes in creating software applications. XYZ signs a contract to develop a complex software solution over a twelve-month period, with a total contract value of $500,000.

As of the end of the eighth month, XYZ Solutions has incurred costs of $300,000, and the estimated total costs for the project remain $400,000. By this time, it hasn’t recognized any revenue, as the project is not yet completed. However, the company has incurred costs of $300,000.

Accrued Revenue: Since no revenue has been recognized yet, and the company has incurred costs, the difference between incurred costs and recognized revenue is considered as accrued revenue. In this case, the accrued revenue is $300,000 (Costs Incurred).

As the project nears completion at the end of the twelfth month, another $300,000 is incurred as costs. At this time, the entire contract value of $500,000 would also be recognized as revenue.

Revenue Variance: In this scenario, the estimated total costs for the project remained at $400,000. However, the actual costs exceeded expectations, totaling $600,000 upon completion. The recognized revenue upon project completion still stands at $500,000.

This outcome results in a revenue variance of -$100,000, highlighting that the project's actual costs overran the initial estimate by $200,000, thereby impacting the project's profitability.

Best Practices for Revenue Recognition

Implementing effective practices that follow the revenue recognition principle is crucial for accurate financial reporting, compliance with accounting standards, and maintaining transparency in business operations. Here are some of the best practices to consider:

Understand Applicable Standards

Familiarize yourself with the relevant accounting standards for your industry, such as ASC 606 or IFRS 15. Stay abreast of any new changes or amendments to ensure compliance.

Regularly Review Contracts

Continuously review contracts to assess changes in terms, scope, or pricing. Adjust revenue recognition as necessary to reflect the updated obligations.

Document and Justify Decisions

Maintain comprehensive documentation of your revenue recognition decisions, methodologies, and judgments. This supports transparency and helps with audits.

Provide Training

Train your finance and sales teams on revenue recognition principles and policies. This ensures everyone involved understands the impact of their actions on revenue recognition.

Regularly Audit Processes

Conduct regular internal audits to validate that revenue recognition processes are being followed accurately and consistently across the organization.

Stay Current

Keep up-to-date with evolving business models, technological advancements, and changes in accounting standards that might impact revenue recognition.

Collaboration Between Departments

Foster collaboration between sales, finance, legal, and operations teams to ensure accurate and consistent revenue recognition across the organization.

Transparency in Reporting

Clearly disclose revenue recognition policies and methods in financial statements. This provides stakeholders with a clear understanding of how revenue is recognized.

Seek Professional Advice

For complex contracts or industries, consider seeking advice from financial advisors, auditors, or legal experts to ensure proper revenue recognition.

Revenue Recognition Software

Organizations also utilize specialized revenue recognition software or integrated Enterprise Resource Planning (ERP) systems to streamline and enhance the accounting processes. These tools provide a comprehensive solution to accurately track, calculate, and report revenue, ensuring consistency and reducing the risk of manual errors.

Replicon offers a robust revenue recognition software solution that empowers businesses to easily navigate complex revenue recognition challenges. Designed to align with evolving accounting standards like ASC 606 and IFRS 15, Replicon provides a user-friendly platform to effectively implement all the above-mentioned revenue recognition best practices.

Conclusion

This page provides comprehensive insights into various aspects of revenue recognition, ranging from key concepts and metrics to different revenue recognition methods. By delving into the nuances of revenue recognition, you can enhance your financial reporting practices and ensure that revenue is recognized accurately and consistently.

Remember that there’s no one-size-fits-all approach; it requires careful consideration of your specific industry, business model, and contractual arrangements. The examples and best practices shared here offer valuable guidance for navigating the complexities of revenue recognition, but tailoring these insights to your unique circumstances is crucial.

NOTE: To ensure accuracy and completeness in implementing revenue recognition in your organization, it’s recommended to refer to specialized resources and financial textbooks or seek assistance from financial professionals experienced in using these methods

Frequently Asked Questions

The five criteria for revenue recognition include:

- identification of the contract with customers

- determination of performance obligations

- agreed-upon transaction price

- allocation of the price to obligations

- satisfaction of obligations leading to revenue recognition

Revenue recognition involves recording revenue in financial statements when it's earned and realizable. For instance, a software company recognizes revenue as customers pay for software licenses, with revenue aligned to the delivery of the software.

Types of revenue recognition include percentage-of-completion, on-invoice, drawdown, as-incurred and equal distribution methods. These methods determine when and how revenue should be recognized based on project progress, contractual terms, and performance.

GAAP Revenue Recognition refers to adhering to accounting standards set by authoritative bodies like the Financial Accounting Standards Board (FASB). These standards ensure that companies report revenue in a consistent and transparent manner, reflecting economic reality and providing accurate financial information to stakeholders.

ASC 606, also called "ASC 606 Revenue Recognition from Contracts with Customers", is a significant revenue recognition accounting standard established by the Financial Accounting Standards Board (FASB). This standard provides comprehensive guidelines for how companies should recognize revenue from customer contracts.