As the state, local and education (SLED) market continues its recovery heading into the 2022 calendar year, it’s important to understand how the market is performing and where it’s headed.

GovWin’s team of research experts recently released a report, the 2022 SLED Government Contracting Forecast, to comment on current SLED market conditions, and hosted a webinar outlining some of the key trends to look for in the months ahead. Below we’ve compiled a summary of both to create a “cheat sheet” to SLED contracting in 2022.

State and Local Government Spending Outlook in 2022

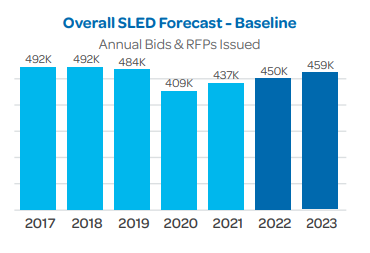

The rebound in bids and RFPs issued during 2021 coming out of the 2020 decline was a little slower than expected. At +6.8% growth, the market is still making substantial progress at returning to normal, just at a slower pace that will likely take several years to catch up after the -15% loss. Generally speaking, it will take a more predictable and stabilized economy – and continued progress with the pandemic - to help state and local entities feel safe enough to hire back missing staff and return to previous buying patterns.

The good news is that bids and RFPs should continue on their upward trend in 2022, reaching 450K (as shown in the chart below) with growth of 3%. This would be followed by an expected increase of another 2% for 2023, continuing the progress made during 2022.

In GovWin’s 2022 SLED Government Contracting Forecast report, our SLED research team has looked at areas where we expect bids and RFPs to be recovering to or near pre-pandemic levels. Based on real bid monitoring of the twelve major industry groups covered in our GovWin platform, only educational products and services has fully recovered to its pre-pandemic level of bidding opportunities. By 2022, we expect to see two more industry areas reach this level – environmental services and healthcare. And by 2023 three more industry areas should have fully recovered to the level of bids and RFPs that were released prior to the pandemic.

Sources of Funding for State and Local Bids and RFPs

An area many government vendors are focused on has been the American Rescue Plan Act. At the state and local level this act adds roughly $220B of coronavirus fiscal recovery funds to flow down to state and local government agencies. Most of this money will be allocated to the 50 states (and the District of Columbia). It also made available nearly $129B for the K-12 Education Stabilization fund.

The recent infrastructure bill could also provide significant funding for state and local projects across a variety of industry areas. Some of the major areas of SLED infrastructure investment in the next five years to come out of this bill will include:

- $110B for roads and bridges

- $66B for rail

- $65B to close the broadband gap

- $55B for clean water and to eliminate lead pipes

- $46B to mitigate floods, wildfires and droughts

- $42B for air/sea ports

- $39B for mass transit

- $28B for electric grid infrastructure

- $7.5B for e-vehicle charging

Other State and Local Government Trends to Watch in 2022

It goes without saying that economic disruption from labor market issues, shortages and supply-side problems is an ongoing development to watch. SLED government officials are looking for evidence that more economic stability has returned, and the more of that they see the more likely that growth will increase.

Government contract consolidation is another ongoing trend impacting vendors at both the federal and SLED levels. Fewer opportunities has made it more valuable than ever for businesses to diversify and expand the types of business development strategies they are utilizing, such as expiring fixed-term contracts and cooperative purchasing vehicles.

Leverage State and Local Government Contracting Trends to Build Your Pipeline

With these key trends for 2022 in mind, do you have confidence on where the U.S. state, local and education government contracting market is headed? Our research team presented an exclusive webinar to dive into the details and provide actionable insights on what you need to know about SLED government contracting for the next 12 months.

When you register for GovWin’s State and Local Government Contracting Trends for 2022 on-demand webinar, you will gain access to research on SLED market conditions and key trends to help you get ahead of the competition and win more government business in 2022. Click the link below to sign up for free.

Deltek Project Nation Newsletter

Subscribe to receive the latest news and best practices across a range of relevant topics and industries.